We care deeply about the success of our clients. We are guided by integrity and a strong ethical obligation to always do what is right and good for those who place their trust in us. We utilize a purpose-based investment approach. We work with our clients to create a financial plan that estimates the cost of their goals. We then segregate their assets into pools that are aligned with their goals. Each pool of assets is allocated, diversified and rebalanced in a manner that is appropriate for their risk tolerance, time frame and objective for each pool.

Markets Work

A cornerstone concept of modern economics is that a free and competitive market system is the most efficient way to allocate resources. Securities markets throughout the world have a history of rewarding investors for the capital they supply. Companies compete for investment capital, and millions of investors compete with each other to find the most attractive returns. This competition quickly drives prices to fair value, ensuring that no investor can expect greater returns without taking greater risk.

We have reached the following conclusions with respect to the public capital markets:

-

Current market prices incorporate all available information and expectations about the future, and are therefore the best approximation of intrinsic value

-

Price changes are generally due to unforeseen events and cannot be predicted with any consistency

-

Pricing errors occur, but they do not do so in predictable patterns and it is difficult to recognize them in real time

We use institutional mutual funds, ETF’s and separately managed accounts that incorporate the following concepts in our asset class investing approach:

Capture Market Rates of Return

-

Attempt to capture market rates of return by investing in large numbers of securities in selected asset classes, resulting in portfolios that offer exposure to thousands of securities (through institutional mutual funds, ETF’s and separately managed accounts).

Exclude Certain Securities

-

Exclude Initial Public Offerings, financially distressed and bankrupt companies, and illiquid securities.

Minimize Trading Costs

-

Own a broad representation of securities in an asset classes and hold onto them, rather than frequently buying and selling unnecessarily.

-

Do not attempt to track indexes as this can result in significant trading costs.

-

Allow portfolio managers flexibility on when to add or remove individual securities from asset classes to account for momentum effects, trading costs, etc.

Asset Allocation

We believe that investment returns are determined principally by risk, and that a diversified portfolio's expected return is a result of its exposure to certain risk market-based factors. Since a portfolio's asset allocation determines its risk factor exposure, how to allocate one's assets into purpose based pools of money is one of the most important decisions an investor can make.

Our research has identified six risk factors that we believe determine the expected rates of return of a diversified portfolio. The first three are stock market risk factors and the last two are fixed income risk factors:

Market Risk

-

Stocks in general have higher expected returns than fixed income securities.

Size Risk

-

Small company stocks have higher expected returns than large company stocks.

Valuation Risk

-

Lower-priced "value" stocks have higher expected returns than higher-priced "growth" stocks.

Profitability Risk

-

Securities with higher profitability have higher expected returns.

Maturity Risk

-

Longer-term instruments are riskier than shorter-term instruments and therefore have higher expected returns.

Default Risk

-

Instruments of lower credit quality are riskier than instruments of higher credit quality and therefore have higher expected returns.

Academic studies show that the degree to which a portfolio is exposed to these five risk factors determines nearly all of its risk and expected return. An advantage of purpose based investing is the ease in which one can manage risk by investing in precise asset classes.

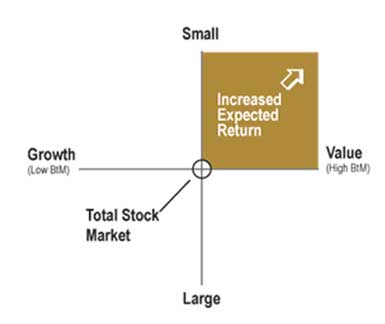

You can visualize the equity risk components with the illustration below. The extent to which you "tilt" your portfolio toward small and value stocks can increase your risk and expected return.

Cross Section of Expected Stock Returns, Eugene F. Fama and Kenneth R. French, Journal of Finance 47 (1992)

Effective Diversification

Successful investing means not only capturing risks that generate expected return but also reducing risks that do not. Avoidable risks include holding too few securities, betting on individual countries, industries, or sectors, following market predictions, and speculating on buy or sell recommendations from securities analysts.

Diversification is the antidote to all of these potentially damaging mistakes. Diversification helps to minimize the random outcomes of individual stocks, and positions your portfolio to capture the returns of broad economic forces.

Diversification is much more than the idea of not putting all your eggs in one basket. We know that stocks that share similar risk factors tend to move together. This can dramatically reduce the benefit of owning multiple stocks in a portfolio. In a simplistic example, if a portfolio of stocks move in perfect correlation, there is little reason to own more than one. Combining stocks in a portfolio that move in tandem is what we call "ineffective diversification" because risk is not reduced.

Alternatively, "effective diversification" does help to reduce risk. An effectively diversified portfolio is constructed of securities, or preferably entire asset classes, that do not share common risk factors and therefore tend not to move in concert with each other. These portfolios have components that “zig” while others “zag,” creating a more consistent, less volatile net return series. Effective diversification should not only help you sleep better at night, but also your money may compound at a greater rate compared to a more volatile portfolio with the same average return.

Combine Multiple Asset Classes

-

Seek to combine multiple asset classes that have historically experienced dissimilar return patterns across various financial and economic environments.

Diversify Globally

-

Approximately 40% of the market value of global equities is located outside the United States. International stock markets as a whole have historically exhibited dissimilar

return patterns to the U.S. markets.

Invest in Thousands of Securities

-

Compared to a portfolio concentrated in a small number of securities, investing in thousands of securities around the world can limit portfolio losses during a severe market decline by reducing company-specific risk.

Invest in High-Quality, Short-Term Fixed Income

-

We believe the role of fixed income in a diversified portfolio is to reduce volatility while producing income. We seek to accomplish this by utilizing short-term, high-quality securities that have a low correlation with stocks and strong credit quality.

Periodic Rebalancing

A portfolio can drift from its initial asset allocation over time due to market fluctuations, changing the portfolio's risk and return characteristics. By rebalancing the portfolio on a regular basis, the original risk profile can be more closely maintained. We review all portfolios regularly for rebalancing.